Traditional lending is often slow and depends on banks and multiple approvals. P2P lending changes this by connecting borrowers and lenders directly through a digital platform.

This model is growing quickly as users look for faster access to funds and better returns on their investments. For businesses, it creates a strong opportunity to build a scalable fintech product with steady revenue potential.

In this guide, we’ll break down everything you need to know, from how P2P lending software development works to the core features, development process, tech stack, and cost involved in launching a fully functional platform.

What Is P2P Lending Software?

P2P lending software is a digital platform that connects borrowers and lenders directly, without involving traditional financial institutions. It works as a lending marketplace where users can either request loans or invest money based on defined terms.

On the borrower side, users can create loan requests by setting details like amount, duration, and purpose. On the lender side, users can review these requests, analyze risk levels, and choose where to invest based on expected returns.

The platform itself handles the full lending lifecycle. This involves user onboarding, KYC verification, credit risk scoring, loan matching, fund disbursement, repayment tracking, etc. It also manages transactions through integrated payment gateways and takes care of data security through encryption and access controls.

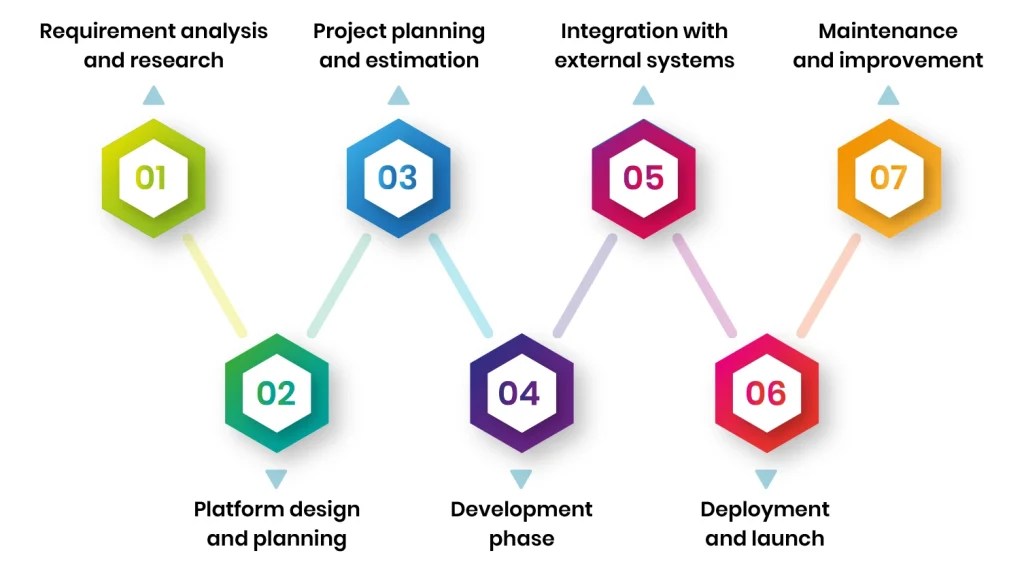

Key Steps to Build P2P Lending Software

Building a P2P lending platform is not just about coding. It requires proper planning, system design, and long-term support. Each stage focuses on making the platform secure, scalable, and easy to use for both borrowers and lenders.

1. Requirement analysis and research

This is the first stage, and it usually takes around 4 weeks. The team studies the target users, both borrowers and lenders. They also analyze competitors in the market. Based on this, they define what features the platform should have. This includes both functional needs and compliance requirements. It helps set a clear direction for development.

2. Platform design and planning

This step usually takes 4 to 8 weeks. In this phase, the system structure is designed. This includes features, workflows, and user experience for different roles. The architecture is planned along with integrations like payment systems and credit APIs. Technology choices are also made at this stage. Sometimes a small prototype is built to test the idea.

3. Project planning and estimation

This stage takes around 1 to 3 weeks. Here, the full project plan is created. This includes timeline, cost, resources, and delivery milestones. Risks are also identified early so they can be managed. The goal is to make sure the project is realistic in terms of timeline and budget.

4. Development phase

This is the main building stage, and it usually takes 6 to 9 months. Developers work on both frontend and backend systems. APIs, databases, and core features are developed. Testing is done during this phase to fix issues early. DevOps practices are also used to manage deployment and automation.

5. Integration with external systems

This step takes around 4 to 8 weeks. This depends on the number and complexity of integrations. The platform is connected with third-party services. These include payment gateways, credit bureaus, and analytics tools. Integration testing is done to make sure all systems work together without any errors.

6. Deployment and launch

This stage usually takes 1 to 3 weeks. Once software development is complete, the P2P lending platform is launched. The infrastructure is set up, and the system goes live. Security, backups, and performance settings are configured before release.

7. Maintenance and improvement

This is an ongoing phase with no fixed timeline. After deployment, the P2P lending platform needs continuous support. Bugs are fixed when they appear. In addition, Updates and new features are added based on user feedback. The system is also monitored to keep it stable and compliant.

Where P2P Lending Software Is Used?

P2P lending software is used in different financial areas where direct lending between users makes more sense than traditional banking. There are 3 main use cases that dominate this space.

Consumer lending

The first and most common use case is consumer lending. In this model, individuals use the platform to get funding for personal needs like education, medical expenses, home improvement, or buying a vehicle.

It works well because approval is usually faster and more flexible compared to banks. Lenders also get attractive returns based on the borrower’s risk profile, which makes it a popular investment option.

Business microloans

The second use case is microfinancing for small and medium businesses. These loans are used for day-to-day business growth needs like purchasing stock, upgrading equipment, or running marketing campaigns.

For businesses, it is easier to raise funds without heavy banking requirements. For lenders, it creates a chance to invest in multiple small loans and spread risk across different businesses.

Crypto lending

The third use case is crypto-based lending. Here, digital assets are used to issue and manage loans through blockchain-powered systems.

Borrowers can access funds without traditional credit checks. Lenders get more transparency and can participate in global lending opportunities with real-time tracking of transactions.

Key Features of a P2P Lending Platform

A P2P lending platform is designed to manage the full lending cycle between borrowers and lenders. It automates onboarding, credit checks, loan processing, payments, and reporting in one system. The features are usually divided based on user roles.

Borrower Side Features

Account setup and loan access

Borrowers can register on the platform, complete KYC verification, and create a profile. They can upload personal or business documents and manage their account details in one place.

Loan calculator and comparison

Borrowers can check different loan options before applying. They can compare interest rates, repayment terms, and total loan cost. Advanced platforms also suggest suitable loan offers based on their profile and affordability.

Loan application and repayment

Borrowers can submit loan requests directly through the platform. They can track approval status in real time. Once approved, they receive funds and manage repayments through scheduled EMIs or manual payments. Also, the system sends automatic reminders for due dates.

Lender Side Features

Investment and loan listing access

Lenders can make their profiles and explore all the available loan listings. They can filter opportunities based on risk level, returns, and loan duration.

Loan terms management

Lenders can define loan conditions such as interest rate, tenure, loan amount, and eligibility criteria for borrowers. This helps them control risk and target the right borrower segment.

Loan origination and funding

The platform automates the loan approval process. It checks loan applications and manages approvals. It also calculates expected returns for lenders. After that, it generates digital loan agreements. Once the loan is fully funded, the system sends the money to the borrower.

Loan portfolio management

Lenders can manage all their loans from one dashboard. They can track each loan’s performance. They can also monitor returns and risk levels. Some platforms use advanced models to identify possible defaults. This helps lenders make better investment decisions.

Admin Features

User management and pre-qualification

Admins handle both borrowers and lenders on the platform. They set rules for user onboarding. They also verify identity using KYC and AML checks. Only verified users can access lending features.

Platform analytics and reporting

Admins can view key platform data in dashboards, including loan volume, revenue, and repayment activity. They can also track user behavior. Some systems provide insights into future lending demand and platform growth.

Security and compliance management

Admins make sure the platform follows financial rules. This includes data protection and fraud monitoring. It also includes secure handling of transactions and user data. Systems are often built to comply with standards like GDPR, PCI DSS, and other regional regulations.

Essential Integrations for P2P Lending Platforms

A P2P lending platform works better when it connects with external systems. These integrations help automate financial operations, improve accuracy, and make the platform more reliable.

| Integration Type | Purpose | Key Benefit |

| Accounting software | Records financial transactions in the general ledger and tracks repayments, interest, and revenue | Ensures accurate bookkeeping and reduces manual accounting work |

| Payment gateways | Handles transactions through banks, cards, and digital wallets like PayPal or Stripe | Enables fast, secure, and seamless fund transfers with instant payment status updates |

| Credit rating platforms | Connects with bureaus like Experian, Equifax, or TransUnion to check the borrower’s credit history | Improves risk assessment and helps lenders make better decisions |

| BI and analytics tools | Converts platform data into dashboards and reports for analysis | Provides clear insights into loan performance, user activity, and business growth |

How Much Does It Cost to Build P2P Lending Software?

The cost of building a P2P lending platform depends on factors like feature complexity, scalability, security requirements, and the number of integrations, such as payment gateways, credit rating systems, accounting tools, and BI solutions.

It also varies based on UI and UX requirements, regulatory compliance needs, API development, and the development approach used, whether in-house, outsourced, or a hybrid model. On average, a custom P2P lending platform can cost between $400,000 and $1,000,000+, depending on how advanced and feature-rich the system is.

How Long Does It Take to Develop a P2P Lending Platform?

The development timeline depends on the size of the project, required features, and system complexity. A basic platform takes less time, while a full-scale solution with multiple integrations and compliance requirements takes longer. On average, it takes around 9 to 15 months to design, develop, test, and launch a complete P2P lending software platform.

What Improves ROI in P2P Lending Platforms?

ROI in P2P lending platforms depends on how efficiently the system runs and how well it connects borrowers with lenders. Small improvements in automation, matching, and user experience can directly increase platform profitability and long-term growth.

Automation that reduces manual workload

A major factor that improves returns is automation. When loan approvals, repayments, and user verification run automatically, the platform becomes faster and cheaper to operate. It also allows the system to handle more users without increasing operational effort. This directly improves efficiency and profitability.

Smarter loan matching between users

ROI also depends on how well borrowers and lenders are matched. A strong system connects borrowers with suitable loan offers based on risk profile, amount, and repayment capacity. At the same time, lenders are shown better investment options. This improves fund utilization and increases platform activity.

Simple and clear user experience

User experience plays a direct role in platform growth. When borrowers can apply for loans easily and lenders can invest without confusion, engagement increases. A clean user interface reduces drop-offs and builds trust. This results in higher user retention and more transactions on the P2P lending platform.

Strong integration support through APIs

APIs help the platform connect with external financial systems. This includes banks, payment systems, and credit data providers. Smooth integration reduces delays in processing and improves system performance. It also makes scaling easier as the platform grows.

Frequently Asked Questions

How secure is a P2P lending platform?

A P2P lending platform is built with strong security layers to protect the confidential data of users and financial transactions. It includes multi factor authentication, encrypted data storage, and real time fraud detection systems. Advanced protections like firewalls and intrusion detection systems also help prevent unauthorized access and attacks.

How is fraud prevented in P2P lending software?

Fraud is controlled through automated monitoring systems that track user activity in real time. The platform uses AI based tools to detect unusual behavior and flag suspicious transactions. API level security controls also ensure that only verified systems and users can access sensitive data.

Is P2P lending software compliant with financial regulations?

Yes, modern P2P lending platforms are designed to follow global and local financial regulations. This involves standards like PCI DSS, GDPR, and CCPA, depending on the region. The system also supports KYC and AML processes to make sure of legal compliance for all users.

Why is regulatory compliance important in P2P lending?

Compliance is important because it protects both the platform and its users from legal risks. Without proper compliance, firms can face penalties and loss of trust. A compliant system takes care of the secure handling of financial data and safe transaction processing.

Can compliance rules change based on country?

Yes, compliance requirements vary from one region to another. A good P2P lending platform is designed to adapt to different regulatory frameworks. This means the platform can operate legally in multiple countries without major system changes.